Odyssey is Datacultr’s platform for managing device financing, companies that offer pay-as-you-go and other financing models, utilize Odyssey to drive successful smartphone affordability programs.

Odyssey offers an innovative approach: An intelligent bank-branded solution that harnesses the capabilities of the customer’s smartphone, digital technology and machine learning to provide an effective early-stage collections strategy.

Icon

Secure

Link the loan to the secured device via an undeletable App

Icon

Engage

Build segmented loan journeys, using rich formats that communicate with the device not a phone number

Icon

Detect

Detect and prevent losses due to fake sales

Icon

Collect

Drive collection efficiencies through highly optimised and digitized early collection work-flows

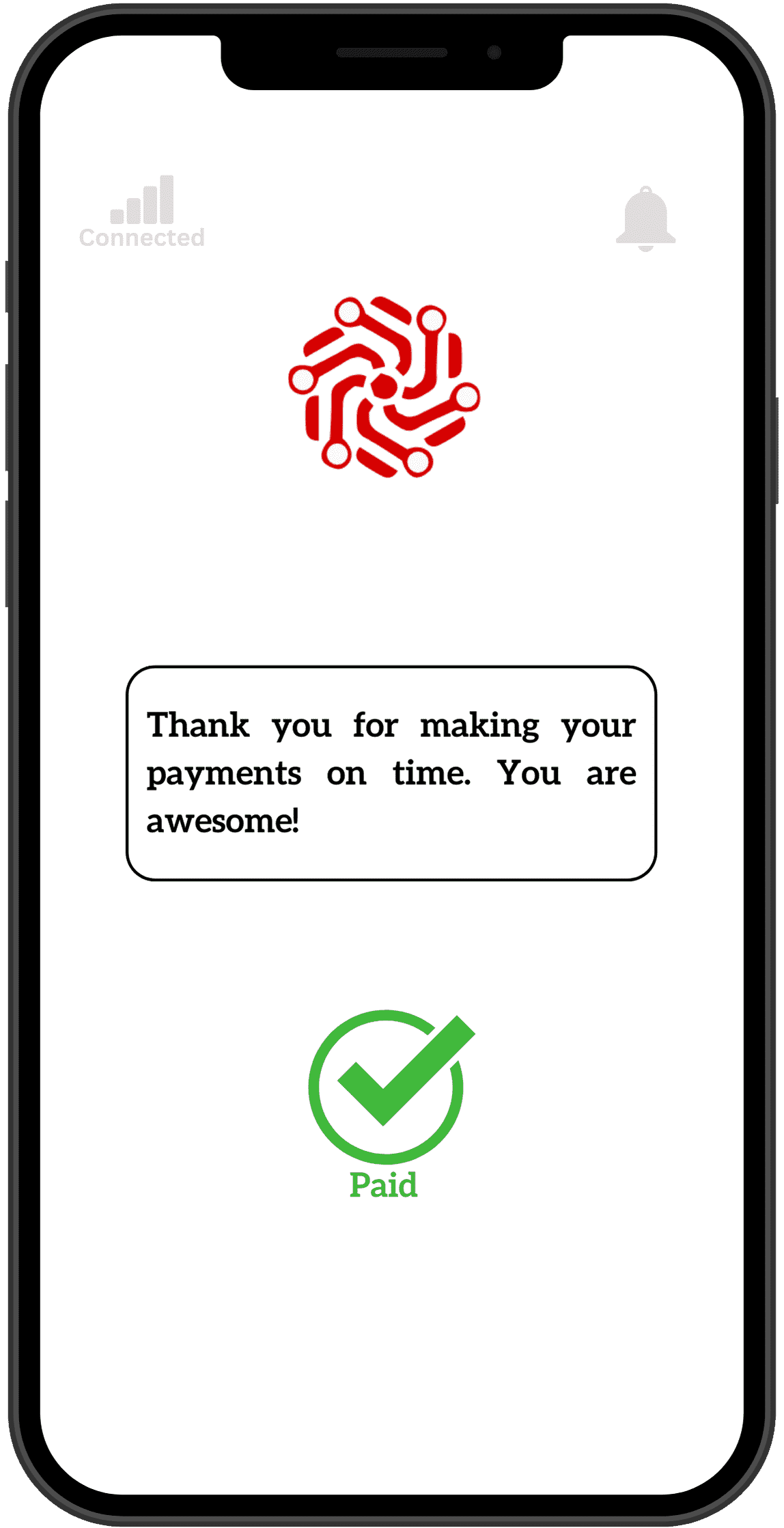

On-Time Payments

Engage with your customers early in the repayment cycle, help the customer understand their loan, and the various payment options that you provide, and educate them about simple financial concepts for a smooth device financing experience.

Often the plain text doesn’t work, use rich videos and banners to deliver your message.

Use high-quality financial education content, thanks to our global partners.

Create a complete digital experience for your customers, how about kicking it off with a welcome call.

Early Debt Collections

Customers prefer digital channels that leverage the fully digital Datacultr platform- digital nudges, automated reminders, and digital workflows for efficient early debt collections in the device financing journey.

Feature

Digital Call-in reminders

Digital nudges including device lock

On-demand services like mobile numbers on-demand

Always connect, by reaching the device

Benefits

Icon

Increase collection efficiency

Icon

Digitalize collection workflows

Icon

Minimize manual interventions

Icon

Reduce cost of servicing

Increase Contactability

Increase Contact-ability in Your Call & Collect Processes

Nearly 70% of contact numbers provided at the time of sale are not in use. Are you also chasing this problem ?

Datacultr’s ON-DEMAND solutions on device financing help drive up contact-ability by:

Increase agent productivity

Reduce Operational Costs

Increase Collection Efficiencies

Fraud Detection & Prevention

Smart fraud detection and prevention features that reduce losses and ensure you run a successful device affordability program :

Reduce losses by identifying fake sales

Prevent unauthorized usage of the device via multi-layer device security

Always on watermark, that ensures the financed device is not resold in the grey market.

Industry-specific features like SIM swap detection for telecom operators and retail chains selling bundled products.

Device Lock

The device lock is a highly effective deterrent, that ensures customers don’t miss their payments. These are also very effectively integrated by clients in their post-due collection journeys, to ensure missed payments are paid.

To run a successful smartphone financing or PayGo program, Datacultr recommends clear and transparent communication at the time of sale and before locking the device. The Odyssey locked screen provides the customer a clear path to unlock, whereby the customer can pay using payment options allowed by the lender, these may be through payment apps, wallets or a USSD-driven option

Datacultr realizes that customers may be offline, the platform allows on-demand device lock

and unlock, even when the device is OFFLINE.

Unlock a powerful

Device financing program

with Odyssey Today !