The opportunities in device financing are immense, but are you prepared for the challenges? Managing risk and ensuring timely payments can definitely make or break your business.

Delinquencies are rising. Is your lending model evolving to stay resilient, or just scaling the risk?

Here’s a crucial insight: the gross bad loan ratio was 2.3% in March 2025 and is expected to rise marginally to 2.5% by March 2027, according to a Reuters report. As bad loans inch higher, how will you protect your portfolio while scaling confidently?

Don’t worry; we have got you covered!

At Datacultr, we’ve worked with leading financial institutions, NBFCs, and telecom operators across 30+ countries, helping finance over 20 million devices worth $5.45 billion. Along the way, we’ve identified the most effective strategies to build a strong and profitable device financing model.

Let’s dive into these best practices:

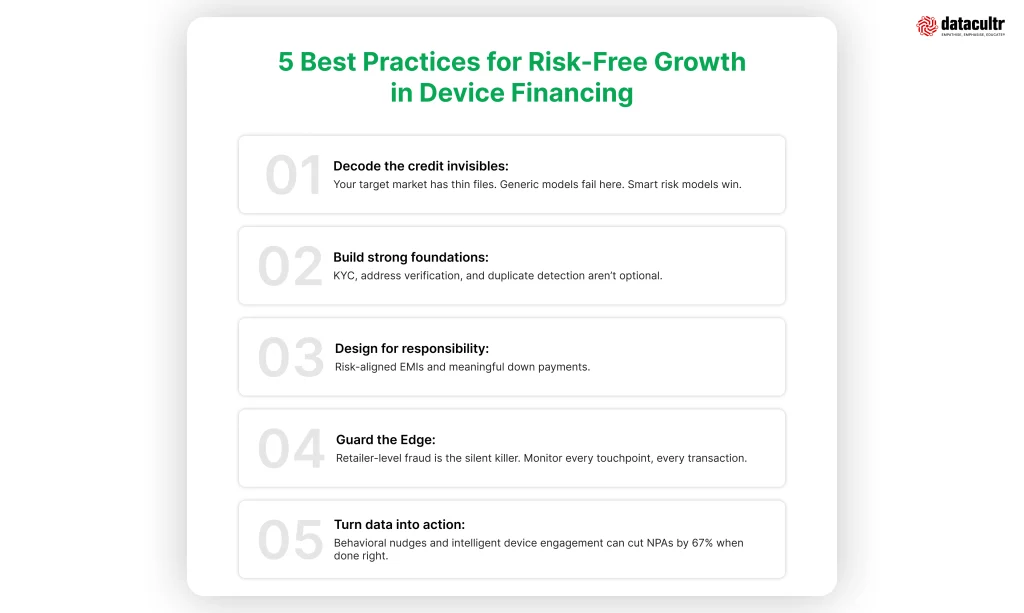

1. Understand Customers’ Credit History to Finance Smarter

Not all borrowers fit the traditional mold. In emerging economies, your target market often consists of “credit invisibles” individuals with thin or non-traditional credit histories, for whom generic risk models simply do not work.

To successfully scale smartphone financing, tablet financing, or TV financing, you need alternative, smart risk models that go beyond traditional credit scores. Assessing income sources, repayment intent, and other behavioral signals is essential, rather than relying only on bureau data. Spot risk markers proactively, such as past defaults or over-indebtedness, and blend these insights into a customized approval process.

Result? A broader customer base, smarter approvals, and significantly lower default rates.

2. Build a Strong Foundation with Customer Due Diligence

Would you build a house on shaky ground? No way. Well, the same principle applies to smartphone financing, and customer due diligence (CDD) is your foundation.

It starts with a positive KYC check. If it fails, it’s an instant rejection. Then comes address verification, done through utility bills or trusted databases, to confirm the borrower’s location and identity. This stage is where fraud often begins. The same ID or address is frequently reused across multiple loan applications, making it critical to flag duplicates early.

Additionally, leveraging data insights, such as the distance between a customer’s home and the store, enables more precise risk assessment.

3. Design a Loan That Balances Opportunity & Protection

Successful loan isn’t just about getting customers through the door; it’s about ensuring they can repay confidently. Studies show that borrowers who contribute at least 30% as a down payment are less likely to default.

Lend smarter, not riskier. The right balance keeps money flowing. Here’s how you can do it:

- Credit Limit: For new-to-credit or thin-file customers, cap the loan amount within 60% of monthly income. This avoids over-lending and keeps repayments manageable.

- Down Payment: Ask for a 25% – 35% down payment to ensure customer commitment.

- EMI Affordability: Ensure monthly repayments do not exceed 30–40% of disposable income to keep repayment friction low.

- Fraud Filters: Add filters for blacklisted PIN codes, flagged addresses, or repeat defaulters to block high-risk applicants.

By following these guidelines, lenders can boost profitability while reducing non-performing loans.

4. Manage Retail-Level Lending Risk

Fraud doesn’t always start with the customers; sometimes, it begins at the store. Retailer-level fraud is the silent killer in device financing. Poor practices like fake sales, where retailers show a loan disbursal, pay the down payment, and then disappear once the lender pays out, can quietly drain your portfolio.

Here’s how to stay ahead:

- Monitoring every touchpoint and every transaction at the retail level to detect and prevent fraud early.

- Ask for payment guarantees to ensure the first 2–3 EMIs are paid, or blacklist retailers who fail.

- Use retailer scorecards to flag repeated delinquencies and suspicious sale patterns.

- Blacklist retailers who consistently enable default-prone customers or bypass onboarding protocols.

Retail oversight isn’t optional; it’s essential to maintain portfolio quality.

5. Turn Data Into Action with Datacultr’s Digital Device Financing Solutions

Take these best practices to the next level with Datacultr’s smart and innovative solutions.

Behavioral nudges and intelligent device engagement can reduce NPAs by up to 67% when done right. Datacultr’s digital debt collection solutions use real-time reminders via videos, banners, and smart nudges to drive behavior change, boost early-stage collections, and significantly improve repayment rates.

Results Our Partners Love

Still wondering if these strategies work? Here’s what our partners in Southeast Asia, Latin America, and Africa are achieving:

25% increase in on-time

payments

67% fewer non-performing

loans

4X growth in early-stage

collections

Grow with Confidence: The Datacultr Way

Take Your Smartphone Financing Business to the Next Level!

Success isn’t about luck; it’s about using the right strategies and tools to stay ahead of the game. Implementing strong due diligence, designing smart loan products, and using digital solutions can completely change your financing model, driving long-term growth.

That’s exactly what Datacultr empowers you to do.

With our Odyssey platform, you’re not just digitizing collections, you’re turning every financed device into a smart asset. From automated nudges to real-time risk monitoring and virtual collateral, Datacultr helps you reduce fraud, improve recovery, and confidently lend to underserved segments.

Already trusted in 30+ markets, we’re not just enabling device financing, we’re redefining how it works.

People Also Ask

How do digital reminders improve repayment rates?

Digital reminders like app notifications and lock-screen banners keep customers engaged and aware of upcoming payments. These timely reminders significantly improve repayment behavior, making them a simple yet powerful way to reduce late payments and non-performing loans.

Why is a down payment so important in device financing?

Down payment shows the borrower’s commitment. Research shows that customers who put down 25-35% upfront are 40% less likely to default. It reduces the lender’s risk and ensures customers have skin in the game. Plus, it helps maintain a healthy cash flow for the business.

What’s the biggest mistake lenders make when scaling device financing?

Rushing to scale without the right checks in place, especially fraud controls, digital engagement tools, and retailer monitoring. Growth without guardrails often leads to high delinquencies and increased costs. The most successful lenders take a platform-based approach from the start, allowing them to scale smarter, not just faster.

Ready to revolutionize your collections strategy? Experience the future with our cutting-edge platform!

✅Unlock Efficiency

✅Boost Recovery Rates

✅Simplify Your Collections Workflow with Our Innovative Solution.

👉🏻Book Your Personalized Demo Today! Don’t miss out on the opportunity to transform your collections process.