Global OS for Risk Management, Digital Debt Collection and Customer Engagement

Datacultr, the leading device financing risk management platform, is now even better with AI-powered customer engagement, delivering the infrastructure to drive digital debt collection, manage risk, and influence behaviour across diverse credit and customer lifecycles.

Book a Demo

Billion+

Check out our Newly launched Transformational AI-driven Digital Customer Engagement Platform

Digital Drives Efficiency, Datacultr Drives Digital Debt Collection

Traditional collection methods have become less effective and more expensive. Across device financing, DaaS, and microfinance portfolios, Right Party Contact (RPC) is declining, and outreach built on calls, SMS, and email is increasingly ignored.

Datacultr replaces the fragmentation by combining device-level control with AI-powered customer engagement. Every communication is delivered, seen, and acted upon, turning financed devices into active recovery and engagement channels.

With Datacultr, Our Clients Achieve

Reduction in First Month Defaults

Reduction in Non-Performing Loans

Increase in Debt Collection Efficiency

Increase in Loan Approvals

Device Financing Risk Management

Device Lock & Risk Mitigation: Mitigate risk across every device financing model with Odyssey

Odyssey, Datacultr's device lock solution, is built for risk mitigation across device financing, Device as a Service (DaaS), and phone as collateral (eezLoan) programs.

When payments are missed, device lock actions are triggered on the financed device, enforcing repayment discipline. Odyssey operates seamlessly across Smartphones, Smart TVs, ACs, Laptops, Tablets, and other Consumer Durables, enabling lenders and OEMs to scale across device categories with built-in risk control.

Device locking and digital workflows for banks, telcos and MFIs

Integration Solutions for OEMs, Retail and Online

BNPL, microfinance, cash loans use case for MFIs using existing phones as collateral

Secure Mono Channel Communication Stack

AI-Powered Customer Engagement: Engage customers, influence behaviour, and drive action with TrueDigi

TrueDigi is Datacultr's AI-powered engagement and digital debt recovery platform for banks and lenders, built to make customer communication more efficient across marketing and collections.

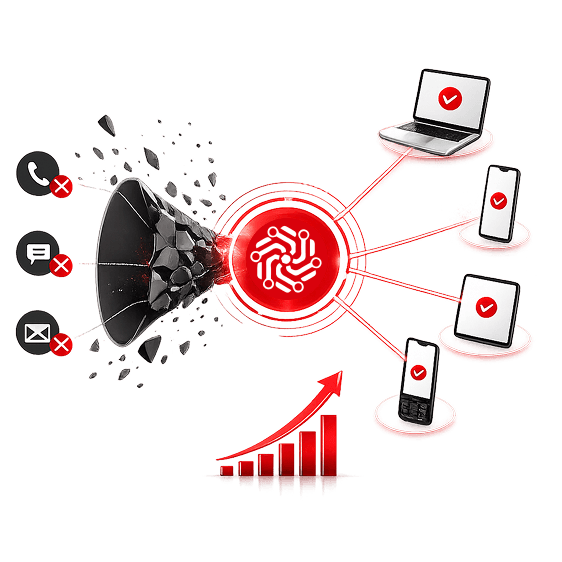

It connects you with the right customer, at the right moment, through the right channel, delivering up to 10x higher engagement. Behavioural AI identifies patterns across the customer lifecycle, enabling proactive engagement that drives repayment action and reduces collection costs.

100%

Promise

Reach customers even when numbers change

Drive immediate response and action

Every message confirmed with a timestamp

Authenticated and secure interactions

Track performance and optimise outcomes

The Datacultr Advantage

100% RPC through guaranteed device-level reach, ensuring every communication is delivered, seen, and acted upon

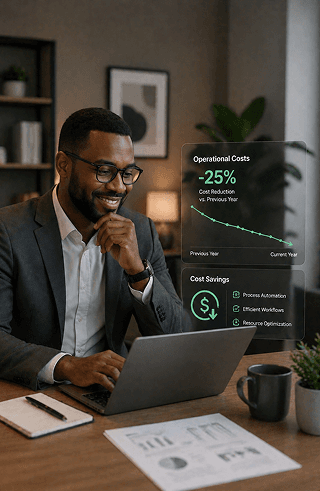

4X increase in collection efficiency across device financing, DaaS, and microfinance portfolios, driving 3X growth in business

Reduce operational costs through automated workflows across collections that strengthen portfolio performance

Turn risk into portfolio growth.

Book a DemoHow Datacultr Supports You Across the Customer Lifecycle

Grow More

Unlock new-to-credit customers and underserved segments with a digital risk infrastructure built to scale financing opportunities.

Engage Better

Engage customers across secure, integrated channels for reminders, updates, and education, driving higher responsiveness and timely actions.

Understand Deeper

Leverage behavioural insights and AI-driven analytics to identify payment patterns and customer activity to make smarter, data-backed decisions.

Collect Faster

Improve collections and mitigate risk with device lock, driving stronger repayment discipline, faster recoveries, and reduced delinquencies.

Grow More

Enable faster onboarding of devices and customer data onto Datacultr's platform with predefined repayment policies to scale operations and grow business from day one.

Engage More

Engage customers across secure, integrated channels for reminders, updates, and education, driving higher responsiveness and timely actions.

Know More

Leverage behavioural insights and AI-driven analytics to identify payment patterns and customer activity to make smarter, data-backed decisions.

Collect More

Improve collections and mitigate risk with device lock, driving stronger repayment discipline, faster recoveries, and reduced delinquencies.

Enterprise Infrastructure, Built for Scale:

A Device-First SaaS Platform

Designed to combine device-level control with AI-powered customer engagement, Datacultr enables businesses to operate and expand across geographies, device categories, and credit models without complexity.

API-First Architecture

Automate and scale the full customer and loan lifecycle with an API-first integration layer, eliminating the need for multiple systems as you grow. Manage workflows and control device & communication actions from a centralised console.

Enterprise-Grade Security & Compliance

Datacultr captures no personally identifiable information (PII) and is fully compliant with GDPR, ISO 27001:2013, and SOC 2 Type II, ensuring secure, auditable operations across markets.

Real-Time Intelligence

Behavioural data is processed and actioned in real time, enabling immediate responses across engagement and digital workflows without operational delays.

Multi-Market, Multi-Device Deployment

Operates consistently across emerging and developed markets, supporting large-scale deployments across diverse device types, customer segments, and credit models.